Resources

Resources

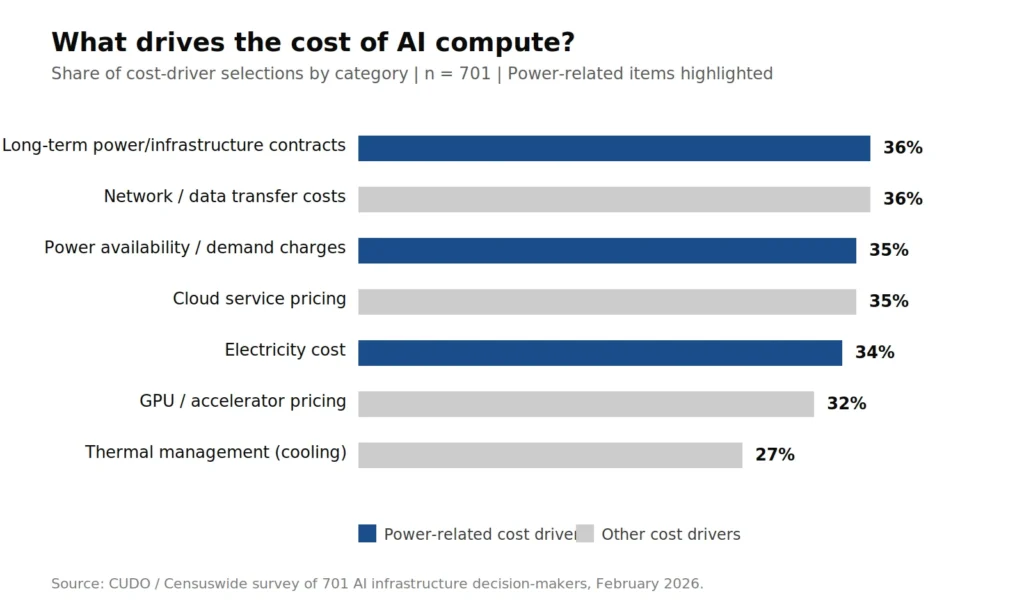

GPU pricing is still the cost most operators plan around, but it is no longer the deciding factor in whether a project is viable. Across 701 infrastructure decision-makers in the UK, US, and Europe, Land. Power. Compute. found that long-term power contracts, network and data transfer costs, and power availability and demand charges now rank as the top three drivers of total AI compute cost. GPU and accelerator pricing ranks sixth. Infrastructure, taken as a category, accounts for 71% of all cost-driver selections.

The practical implication is that two operators buying identical Blackwell allocations at the same price can produce very different cost bases depending on the power contract underneath the facility. One is protected by a fixed-price agreement signed when firm capacity was still available; the other is absorbing whatever the market charges this quarter. That gap does not close with better hardware, scheduling, or utilisation. It closes only with a contract, and contracts of the duration that matter are becoming harder to sign.

This piece explains why that has happened, why the advantage it creates is harder to replicate than the advantages the AI industry has been focused on, and what operators without contracted power should be doing now.

Why GPU advantages don’t hold

The GPU market is transparent, time-bounded, and structurally different from the power market in ways that matter for long-term cost planning. Pricing converges across buyers of similar scale, allocations rotate, and new architectures ship on a roughly annual cycle.

Older generations retain useful life — particularly for inference — but frontier operators consistently prioritise the latest hardware for training and large-scale deployment. The competitive window at the frontier for any single generation is narrow, typically twelve to eighteen months before the next architecture ships.

The operator who paid a premium for early access to one architecture is not holding worthless inventory, but the performance gap between generations narrows with each new release, and the capital bill for staying at the frontier rises with every cycle. A hardware advantage sustained for four quarters is a long one by the standards of this market.

Hardware efficiency gains at the architecture level do not change this dynamic. They compress the cost per token across the entire market at roughly the same rate because every operator buys from the same suppliers. What an operator pays for electricity does not compress in the same way.

Read the full report at cudocompute.com/land-power-compute.

Power doesn’t behave like GPUs

Industrial electricity is locally priced, regulated, and supply-constrained. Prices do not converge globally. Availability at any given price is finite, and in the markets where AI workloads concentrate, it is declining.

- Grid connections are not available on commercial timelines: In European legacy hubs, connecting a data centre to the grid takes an average of seven to ten years. In the UK, projects can wait up to fifteen years, driven by physical reinforcement works and a connection queue that speculative applications have clogged. National grid upgrades that would unblock many of these projects are not scheduled until 2030 or 2031.

Some markets have stopped accepting new applications altogether. Dublin imposed restrictions after data centres reached 22% of total Irish electricity consumption. Amsterdam introduced its moratorium in 2019. Singapore paused new large-load applications between 2019 and 2022.

- Long-lead equipment compounds the problem: Transformers and high-voltage switchgear now take 18 to 24 months from order to delivery. As Tim Dyche, CUDO’s Head of Infrastructure, put it: “If you haven’t placed those orders before you’ve finalised your site, you’ve already lost a year. The supply chain for mechanical and electrical plant is the constraint that sits underneath the power constraint.” Securing a grid connection date means nothing if the switchgear needed to receive the connection is still in a manufacturer’s queue.

- Firm, low-cost power is being contracted out of the market faster than it is being built: Over the past two years, hyperscalers have signed long-duration agreements at unprecedented scale. This looming supply deficit has forced major energy consumers to look beyond traditional grid expansion and actively invest in alternative, dedicated baseload generation.

Consequently, small modular reactor developers have moved from the conceptual stage to pre-order positions, though the timeline remains long. Kinda Sandy, Strategic Director in Oil, Gas and Petrochemicals, told us, “SMRs are not a near-term fix, but they are increasingly being treated as the long-term answer for power-intensive industrial sites.”

The same hyperscalers signing nuclear PPAs today are placing early bets on SMR capacity they won’t receive for a decade. Every gigawatt signed under a multi-decade contract is a gigawatt no longer available to operators arriving two years later.

Taken together, these three constraints– queue length, equipment lead time, and contracted capacity– mean that the cost of power for any given AI facility is largely decided at the moment the contract is signed. Operators who signed in 2023 and 2024 are running facilities at cost bases that cannot now be replicated. Operators signing in 2026 are securing positions that will not be available to anyone arriving in 2028.

What a long-term power contract actually does

A power purchase agreement of fifteen to twenty years at a fixed or capped price does three things that hardware cannot do.

- It converts the most volatile line item on the cost base into a fixed cost: Electricity pricing moves with gas markets, carbon prices, grid-balancing costs, and capacity auction outcomes. Anushka Devaser, Technical Director of Sustainability Advisory at WSP, described the logic operators are applying when they sign: “Predictable power pricing may start higher but protects you over time by flattening the volatility risk.”

The premium paid for a fixed price is insurance against wholesale price spikes during the contract period, and, for AI workloads running at high utilisation for the life of the facility, that insurance compounds.

- It allows the operator to offer price certainty downstream: An operator with a twenty-year power contract can price a five-year compute product with genuine confidence about the cost of delivering it. Jack Halstead, Chief Commercial Officer at Novara Infrastructure, put the commercial consequence directly: “Price certainty will make your customer’s CFO your best friend.” An operator absorbing spot-market movements cannot credibly match that offer, regardless of how favourably it procured its hardware.

- It collateralises the project for debt financing: Infrastructure-style debt is underwritten against contracted cash flows with creditworthy counterparties. Without a long-term offtake and a long-term power contract, the capital required to build at scale is not available at sensible terms. The debt market treats open power positions as market risk rather than project risk, and prices accordingly.

None of these benefits accrues to operators with short-duration power contracts or spot-market exposure. The split between contracted and uncontracted operators is not a matter of preference or procurement style. It is a different cost structure and a different financing profile.

The contract advantage is structurally hard to match

The AI industry has spent the last three years discussing competitive advantage in terms that assume the advantage is replicable: data can be collected, models can be trained, and distribution can be built. All of these are things another operator can do in parallel.

A long-duration power contract is different. The capacity it underwrites is finite. Once a gigawatt is contracted from a given generator for twenty years, that gigawatt is not available to a competitor signing two years later on the same terms. The competitor can sign for different capacity, at a different price, from a different source, often at worse terms. What the competitor cannot do is acquire the original contract.

This is why the position hyperscalers are taking on PPAs is worth watching. They are not simply securing their own cost base; they are removing capacity from the open market for the duration of the contract. For operators arriving behind them, the menu of available contracts is shrinking on two dimensions: fewer creditworthy counterparties are willing to sign, and the prices on offer are less favourable. The arbitrage window that allowed new entrants to secure competitive power in 2023 is narrower in 2026 and will be narrower still in 2028.

The survey data shows operators are already moving in response. 33.7% of respondents now cite power availability and grid capacity as the leading factor in AI workload location decisions. 96% report having adjusted their approach to AI infrastructure location in response to geopolitical and grid conditions. 20% have moved AI workloads out of the UK specifically because of high energy costs — a figure that rises to 26% among AI-first companies. Where power is being located is increasingly where AI is being located.

What operators without contracted power should be doing

Operators who do not already have long-duration power secured have three options, each with specific trade-offs.

- Behind-the-meter generation: On-site generation — gas turbines, CHP, hydrogen fuel cells, or private-wire connections to a nearby generation asset — bypasses the grid queue entirely and removes the network charge from the delivered cost of electricity.

In high-cost markets, this route is often materially cheaper than grid power, even before accounting for timelines. Halstead described the commercial effect: “In markets with high power costs (such as the UK) behind the meter generation will invariably be cheaper than grid power, meaning the commercial proposition to the end user is more attractive to market peers and allows the DC to compete on an international stage.”

The trade-offs are real — gas generation carries environmental and planning friction, hydrogen remains expensive, and private-wire connections require easement agreements from every intervening landowner, with a single holdout capable of killing the route. But in markets where the grid timeline exceeds the project timeline, behind-the-meter is the only route to deliver power within a commercially relevant window.

- Co-development with utilities: Rather than waiting in a grid queue, some operators are entering joint investment arrangements with utilities, committing capital upfront in exchange for firm delivery timelines, phased energisation, and reinforcement commitments. This route is slower than behind-the-meter but carries stronger long-term reliability guarantees and keeps the operator connected to a grid that can absorb load fluctuations. It is capital-intensive at the front end and requires operators to understand utility procurement processes that most are not structured for.

- Acquisition of contracted capacity: As capital constraints bite in the next cycle, some current contract holders will become distressed sellers. Operators with balance-sheet strength may be able to acquire contracted capacity from operators who cannot finish their builds. This is the slowest route of the three and depends on conditions that haven’t materialised yet, but it is one that infrastructure buyers should be monitoring.

All three routes share a now-non-negotiable requirement: power must be sequenced before compute, not after. The prevailing pattern, which is to secure the GPU allocation, then work backwards to the facility, then the power, was viable when grid connections took months. It is not viable when they take seven to fifteen years. Ben Stirk, Head of Enterprise and AI at Ark Datacentre, described the cut-off plainly in the report: “If you don’t already have power secured for a site, or if you haven’t already placed the orders to get it there, you aren’t just behind. You aren’t even in the race.”

What to plan for

For operators still shaping their infrastructure strategy, the priority order is operational rather than strategic:

- Treat power as the first-sequenced decision, not the last: Site selection, contract duration, and equipment procurement should be resolved before the compute footprint is fixed, because those three items determine what the compute footprint can actually be. Halstead’s summary of what a 2027 build requires was direct: “I hope they’ve locked in their power solution already for 2027.”

- Order long-lead equipment in parallel with securing the connection: Transformers and high-voltage switchgear ordered after the grid offer is accepted will not arrive in time. The procurement timeline for mechanical and electrical plant needs to run alongside the power timeline, not downstream of it.

- Match the contract duration to the facility, not the hardware cycle: Power contracts of 15 to 20 years are the right duration for assets that will host multiple GPU generations. Procurement strategies built around annual or five-year power contracts leave the cost base exposed to volatility that the facility will outlive.

- Structure financing around contracted cashflows from day one: Infrastructure debt is available for projects with contracted offtake and contracted power. Equity-funded builds without those contracts in place are increasingly difficult to refinance, and the window in which open-position projects could raise capital on a compute thesis alone is closing.

- Monitor the contracting activity of larger operators: Hyperscaler and AI-first PPA activity is the leading indicator of which markets will have spare firm capacity available in three to five years and which will not. Markets where the major buyers have locked up the available firm output are the ones where mid-market operators will face worse terms on the remaining contracts.

The cost of AI at scale is being decided outside the discussion that most of the market is still having. The headline metric is no longer the GPU price. It is the terms of the power contract underneath the facility, the lead time on the switchgear that connects it, and whether either exists at all. Operators planning for 2027 and beyond are not competing on silicon. They are competing on whether the megawatts they need have already been signed to someone else.